5.1 Price stability, inflation, deflation

The monetary policy objective of maintaining price stability is not about the stability of individual prices. Instead, the aim is merely for prices to remain stable on average. This means that price increases for some goods balance out price decreases for others so that the price level in the economy as a whole does not change and purchasing power thus remains intact.

Price formation through supply and demand

In a market economy, prices must be flexible.

For a market economy to function smoothly, prices for goods and services must be flexible. Only then do they indicate the scarcity of goods (signalling function) and balance out supply and demand (market-clearing function).

When making purchasing decisions, most people pay attention to the quality, appearance and functionality of the desired goods. However, the price is often just as important. As a rule, the cheaper the product, the greater the demand – as demonstrated by the effect of special offers, for example. It can therefore be said that if the price of a product falls, demand usually rises, as long as all other conditions remain the same. Conversely, if the price rises, demand falls accordingly.

What is true for the demand side also applies to the supply side – just in the opposite direction: if the price rises, the supplied amount usually does too. Existing suppliers will increase production when selling prices rise. At the same time, new suppliers enter the market over the medium term to benefit from the improved business opportunities. However, if the price falls, it is no longer as lucrative to produce the goods in question; thus, supply decreases as well. Some less competitive suppliers will actually stop selling these now unprofitable goods entirely.

Flexible prices ensure a balance between supply and demand.

This “price mechanism” ensures a balance between the amount supplied and the amount in demand, provided that prices can move freely. The price will stabilise at the level where demand for a given good corresponds exactly to its supply. Free price formation creates a balance between supply and demand.

Price stability

We talk of “price stability” when the price level only changes a little over time, even if individual prices rise or fall.

Price stability: the price level should remain stable.

An increase in the price level is called inflation (from the Latin “inflare”, meaning “blow into”, “puff up”). The percentage increase in the price level between two points in time is called the rate of inflation or the rate of price increase. It is usually reported on an annual basis and thus reflects the change compared with the situation 12 months earlier. For example, if a newspaper states that the rate of inflation was 4.9% in January 2022, this means that the price level was 4.9% higher in January 2022 than it was in January 2021.

The opposite process, i.e. a decline in the price level, is called deflation. The percentage decrease in the price level between two points in time is therefore referred to as the rate of price reduction or rate of deflation. However, it is often referred to – paradoxically, in fact – as a negative rate of price increase or a negative rate of inflation. However, deflation is only said to exist if the price level falls not just briefly but over a longer period of time.

If a positive inflation rate declines over time – for example, it falls from 3.6% to 2.5% and then to 1.3% – but stays positive, it is referred to as a falling inflation rate, declining inflation or “disinflation”.

Price level and purchasing power

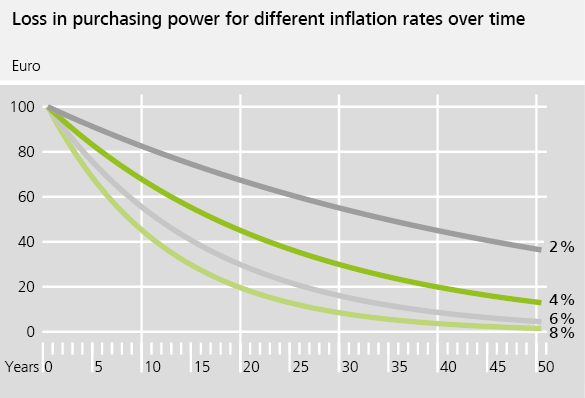

When the price level rises, the value of money falls. In other words, the purchasing power of money decreases as the price level rises because fewer goods and services can be purchased for a given amount of money than before. It can also be said that real monetary value, i.e. monetary value measured in units of goods, declines as a result of inflation. Viewed over a longer period, the loss in purchasing power can be considerable, even if the inflation rate may seem fairly low at first glance. As illustrated by the chart, at an annual inflation rate of 4%, €100 ten years from now would only have the purchasing power of just under €68 today. After 50 years, you would only be able to purchase goods worth the equivalent of €14 today.

Causes of inflation and deflation

In the shorter term, changes in the price level are due to aggregate demand and supply. If aggregate demand increases, this generates price pressures, i.e. inflation, if all other conditions in the economy remain unchanged. This is called demand-driven inflation.

In the shorter term, inflation is determined by supply and demand.

There may be a number of reasons for this. For example, enterprises could be more confident about the future, discover new business opportunities and, accordingly, increase their investment in machinery and equipment or in research and development. Enterprises’ increased demand for investment might also be motivated by lower interest rates, which make loan-funded investments cheaper, and thus more likely, than when interest rates are higher. Households, too, often base their spending on changes in their financing conditions. If interest rates fall, household demand generally also increases. This connection is particularly relevant for the economy if falling interest rates lead to an increase in demand for higher-priced durable goods, such as kitchens or cars. Large amounts of money are usually needed to finance these purchases and are often obtained through loans. Another possibility is that an increase in aggregate demand may be due to higher government demand for consumption and investment or to rising foreign demand (exports).

However, if aggregate demand declines, the opposite holds true. Falling demand tends to lead to reduced price pressures and thus also to falling inflation or, in rare, extreme cases, to persistent, crisis-like deflation.

Changes on the supply side also have an impact on the price level. Since these supply-side changes are usually associated with cost changes, this is called cost-push inflation. One example would be higher production costs as a result of rising energy prices because energy is needed to produce almost every good in an economy. Disrupted supply chains can also significantly increase input costs for enterprises. Wages are likewise an important cost component for enterprises. Enterprises will usually try to pass on their increasing costs to consumers. Higher production costs are therefore often followed by rising prices, leading to cost-push inflation.

In the longer term, inflation is always a monetary phenomenon.

In the long term, a growing supply of money has an impact on price developments. This is because a sustained rise in aggregate prices can only occur if the increase in prices is “financed” by a corresponding increase in the money supply. While not every excessive increase in the money supply necessarily leads to higher inflation, persistently higher inflation always goes hand in hand with excessive growth in the money supply. Thus, one decades-old economic principle is that, in the long run, inflation is ultimately always a monetary phenomenon (from the Latin “moneta”, meaning “mint”, “minted money”). In the long term, inflation is therefore always connected with money and the development of the money supply – a principle that is borne out by many academic studies.

Hyperinflation: inflation out of control

A period in which inflation is already very high, yet keeps rising until it eventually spirals out of control, is called hyperinflation. Hyperinflation generally spells the end of the monetary system. In such a period, money loses its functions, no longer serves as a means of payment, unit of account or store of value, and is no longer accepted by most people. Although there is no universally accepted definition, inflation rates of more than 50% per month are considered a sign of hyperinflation. A monthly inflation rate of 50% means that, over the course of a year, prices rise to more than one hundred times their original level, with money thus losing more than 99% of its purchasing power.

In 1923, Germany suffered hyperinflation, and this became the formative experience of an entire generation. This followed on from the First World War, when the government instructed the Reichsbank to grant it unlimited credit, enabling it to finance around one-third of the war’s cost by printing money.

The volume of banknotes in circulation consequently rose from 2.6 billion to 22.2 billion Mark between 1914 and 1918. The Mark lost value and prices rose. After the war, the Weimar Republic continued this borrowing policy, financing around three-quarters of its expenditure by selling debt securities to the Reichsbank. The money supply grew ever larger. At the same time, the Mark lost its purchasing power. By mid-November 1923, at the height of hyperinflation, the price of a loaf of bread had gone up to more than 230 billion Mark. During hyperinflation, prices rose faster than the Reichsbank could print new banknotes. As a result, cities, local governments and firms began producing emergency money (“Notgeld”) – sometimes with the Reichsbank’s approval, sometimes without. When hyperinflation ended in November 1923, 496 quintillion Reichsmark were circulating as banknotes and 727 quintillion Reichsmark as Notgeld banknotes.

To put an end to inflation, the German government carried out a currency reform in November 1923. Rentenmark banknotes were issued by the Rentenbank, which was established specifically for this purpose. The total volume was limited to 3.2 billion Rentenmark. From 20 November 1923, people could exchange the inflated Mark for Rentenmark at a rate of one trillion to one. The Rentenmark was kept stable by a monetary policy that was strictly oriented to preserving the value of money and consolidating public finances.

However, hyperinflation is not just a phenomenon from the distant past. It can happen again any time, even today. In November 2008, for example, Zimbabwe experienced a period in which prices doubled every 24.7 hours. The government had banknotes printed in ever larger denominations (up to a value of 100 trillion Zimbabwean dollar), fuelling inflation more and more, and was forced to abandon the Zimbabwean dollar in February 2009. In Venezuela, too, the currency depreciated at an increasingly rapid pace over several years. According to the Central Bank of Venezuela, the inflation rate was just over 130,000% in 2018.

5.2 Measuring general price developments

Changes in the price level cannot be measured using individual prices.

Whether the price level and thus the purchasing power of money are changing cannot be measured using just a few prices. It is the average development of all prices in an economy that is important. However, it is virtually impossible to collect millions of individual prices for all goods and services. Therefore, the price developments of a suitable selection of goods are used to determine the change in the price level.

Basket of goods as a basis for the consumer price index (CPI)

Developments in the price level are determined using a basket of goods.

The German Federal Statistical Office (Destatis) determines which goods should be included in the representative “basket of goods” on the basis of a regular sample survey of income and expenditure. The basket comprises around 650 types of goods assigned to 12 categories, covering a wide range of goods and services that are typical of an average German household’s consumption behaviour. The basket contains a wide variety of items, such as food and clothing, housing rents and insurance premiums, as well as services, such as visits to the hairdresser, and occasional purchases like cars and washing machines. It also includes things that are not everyday purchases for everyone, such as prices for a cable car ride, a fishing license and funeral services.

The basket of goods is updated continuously in order to ensure that the price measurement always includes product variants that are currently relevant. Within a product category, the specific individual products for which prices are recorded (known as the price representatives) are therefore replaced regularly. All in all, every month the Federal Statistical Office records over 300,000 individual prices at retailers, in catalogues and on the internet. When measuring prices, it records acquisition costs inclusive of value added tax (VAT) and excise taxes.

Model calculation of a price index

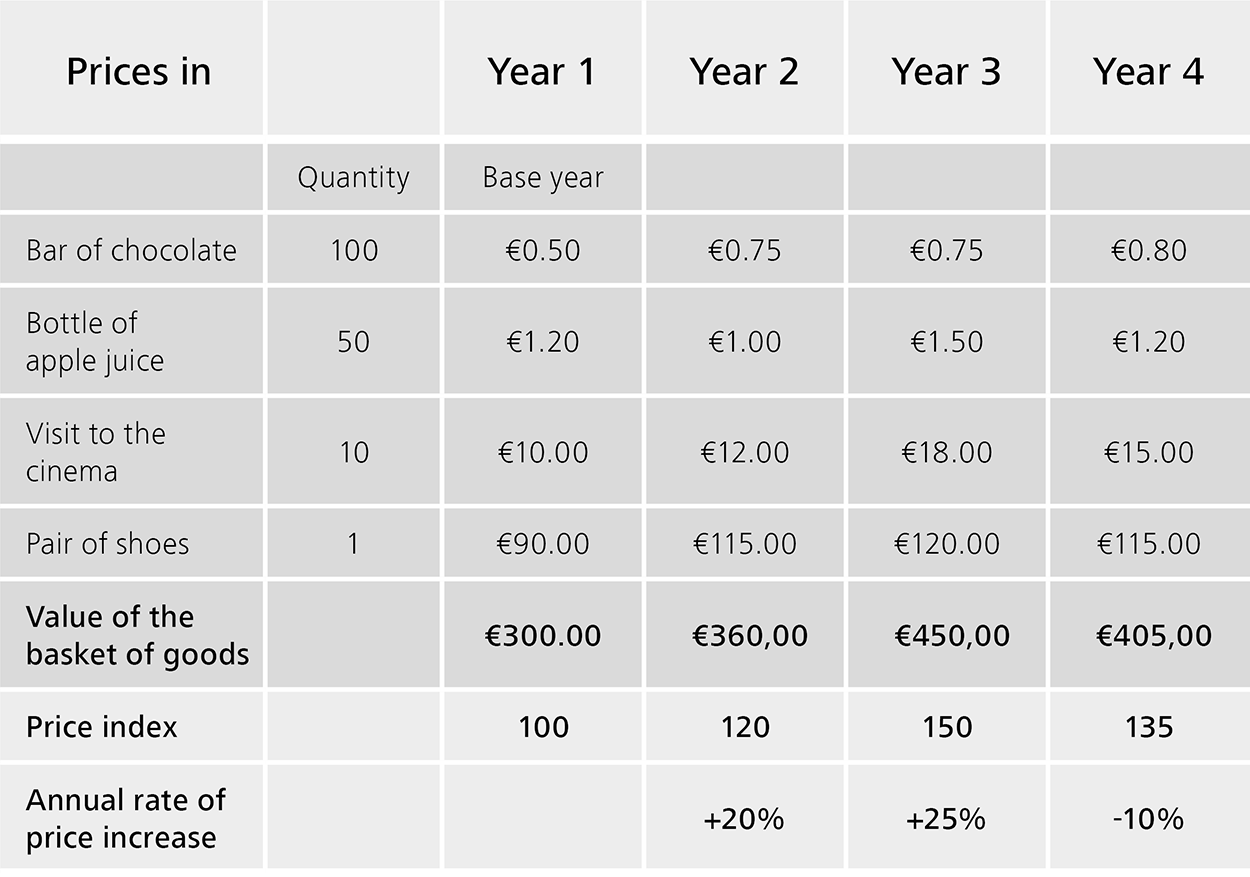

This simplified example illustrates how a price index is calculated and how general price developments are measured. Assuming that a representative basket of annual household expenditure consists of 100 bars of chocolate, 50 bottles of apple juice, 10 visits to the cinema and one pair of shoes, the price index would be calculated using this basket of goods as shown in the table.

The price of the basket of goods is calculated by multiplying the quantity of each good by the respective price and adding the results together (expenditure total). If the basket of goods contains a large number of prices, it is no longer feasible to use the expenditure total; changes are instead indicated using the price index. To do this, the expenditure total of the first year (base year) is set to 100 (€300 equates to 100). This value serves as a reference figure for the following years. The inflation rate represents the relative price change compared with the previous year. As the example shows, the price index can also rise even though individual prices fall.

Changes in quantity are also taken into account when measuring prices.

The official price measurement takes into account not only the specified price but also any changes in quantities. This means that if the amount of product in a package has changed but the quality and price have remained the same, the statisticians carry out a quantity adjustment to ensure that the price is measured correctly. In other words, if, for example, the same product has the same price as before despite its quantity being reduced (e.g. a smaller amount in each package), this is recorded as a “hidden” price increase. The price adjustment method described here is typically applied to food and other non-durable goods.

The Federal Statistical Office uses the prices of the goods in the basket to calculate the consumer price index (CPI) in Germany on a monthly basis. This measures the average change in the prices of all goods and services purchased by households for consumption purposes. The annual change in the consumer price index, i.e. compared with 12 months earlier, is expressed as a percentage and is called the inflation rate. The change in the CPI is the value to which journalists refer when talking about the inflation rate in Germany.

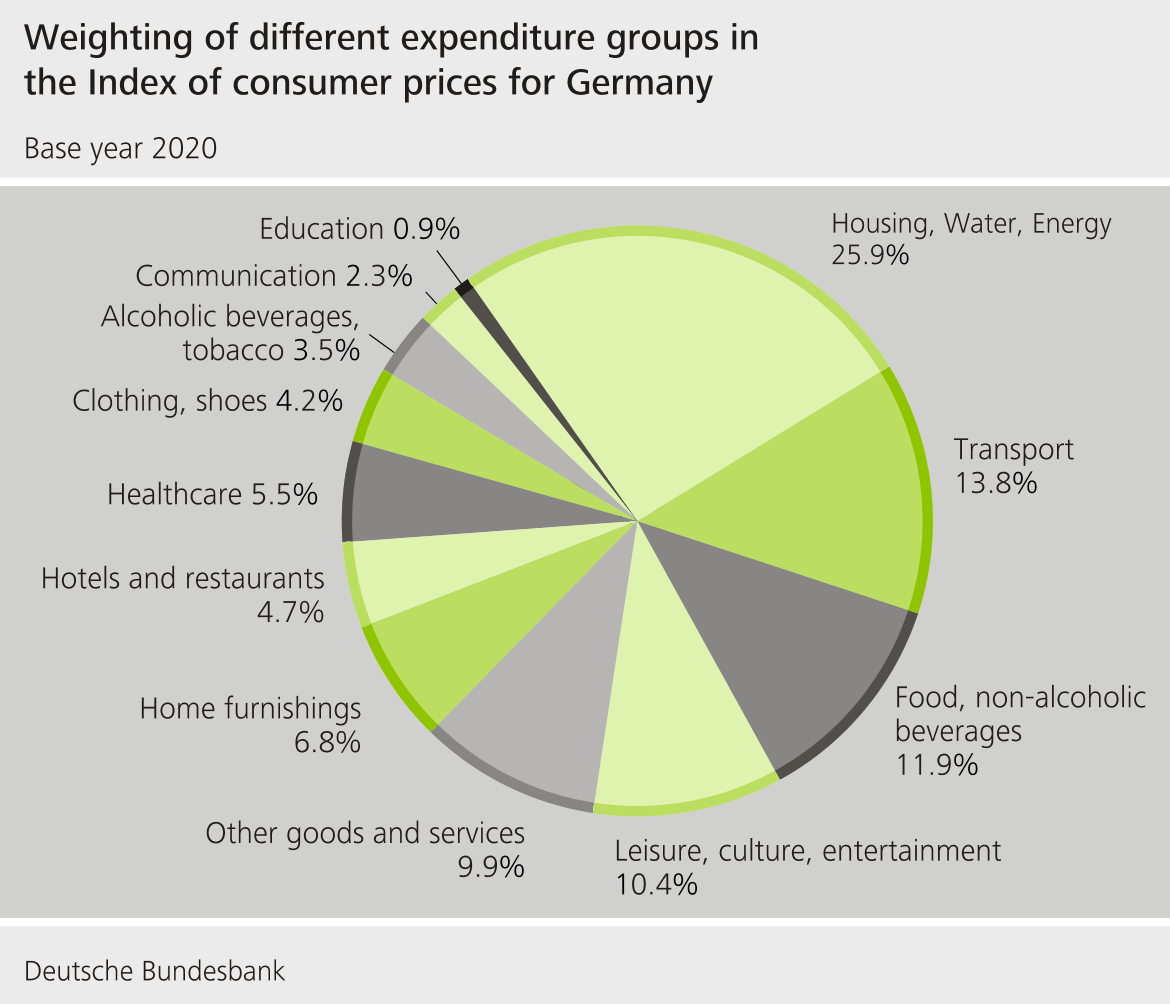

The weighting scheme

The higher the expenditure share of a goods category, the greater the impact on the price index.

When calculating the consumer price index, the price changes of the individual types of goods are weighted differently. The higher the share of consumption expenditure that is accounted for by a particular category of goods, the more clearly the price index reflects the changes in their prices. The weighting scheme determines the respective expenditure shares and thus the weights of the individual goods categories for the index calculation.

The basket of goods is continuously updated at the individual product level. By contrast, the Federal Statistical Office deliberately keeps the weighting scheme of a base year constant for five years when calculating the consumer price index since the price index should only reflect the price changes and not changes in consumption habits. It would no longer be possible to identify price changes in isolation if the expenditure weights were also changed on a monthly basis in the official price measurement, i.e. if “purchasing behaviour” were to change continuously.

How price measurement takes into account changes in quality

In the official price statistics, price changes should be measured in such a way that they remain as unaffected as possible by changes in the quality of the goods or services. Thanks to technological advances, however, many products are constantly undergoing further development and, in many cases, being improved. Therefore, after a certain period of time, it is no longer possible to purchase many goods in their original form – advances in mobile phone technology over the past 20 years are a prime example. Should an enhanced product supersede a product previously included in the consumer price index, statisticians need to apply specialised quality adjustment methods so that they can evaluate the measured price change in a meaningful way.

Quality changes must be factored out for price measurement to be correct.

When it comes to correctly measuring inflation, quality changes are relevant for the following reasons. If the prices of monitored goods rise at the same time as their quality, it is necessary to distinguish between the “pure” price increase and the price increase attributable to the improved quality. In such cases, the price differential caused by the change in quality is estimated and factored out when calculating the consumer price index. In other words, if the price has only risen for quality reasons, this does not signify a loss of purchasing power, as consumers now also get “more for their money” than before with the new, improved product. Using quality adjustment procedures therefore ensures that, despite product changes, like is compared with like when prices are measured. In this way, the calculated price changes can then be interpreted as “pure” price developments and distinguished from quality-related price changes.

Quality adjustment procedures

In the face of the often changing product quality, statisticians have developed a variety of methods to adjust measured price developments. Not all adjustment procedures are applied at the same time. Instead, a suitable set of methods are applied.

Quality adjustment can be achieved by identifying monetary benefits, for example. This means that by including supplementary sources of information for some products an evaluation can be made of the specific additional benefits – measured in financial terms – that a new product model offers. The increasing efficiency of technical devices and appliances is a case in point. Taking the example of a new washing machine, statisticians factor the monetary benefit from the lower electricity and water consumption out of the price of the washing machine.

Another method of taking quality differentials into account is to use the prices paid for optional extras. Statisticians tend to use this adjustment procedure if a certain product feature was originally an optional extra but now comes as standard, such as park assist devices installed in cars. In such cases, part of the amount that, according to the list price, would once have been paid for the optional extra can then be recognised as the monetary value of the quality differential and thus factored out of the price change.

Using hedonic methods, it is possible to calculate the impact of individual product features (such as memory size and processing power) on product prices. In particular, these methods are used to perform quality adjustment for products which undergo changes within a short space of time (computers and smart phones, for example). The frequent price changes seen for such products are often also accompanied by product upgrades. Hedonic methods make it possible to calculate the monetary value of the quality differential between the old and new models, distinguishing it from the "pure" change in price.

The HICP: The measure of price stability in the euro area

The primary objective of the Eurosystem’s monetary policy is to maintain price stability in the euro area. A metric is therefore required to measure average price developments across the entire euro area. This is the Harmonised Index of Consumer Prices (HICP), which every euro area country derives from its respective national consumer price index following a common methodology. In Germany, the rate of change in the HICP usually differs from the inflation rate as measured by the CPI by only one- or two-tenths of a percentage point.

The HICP is the key measure of price stability in the euro area.

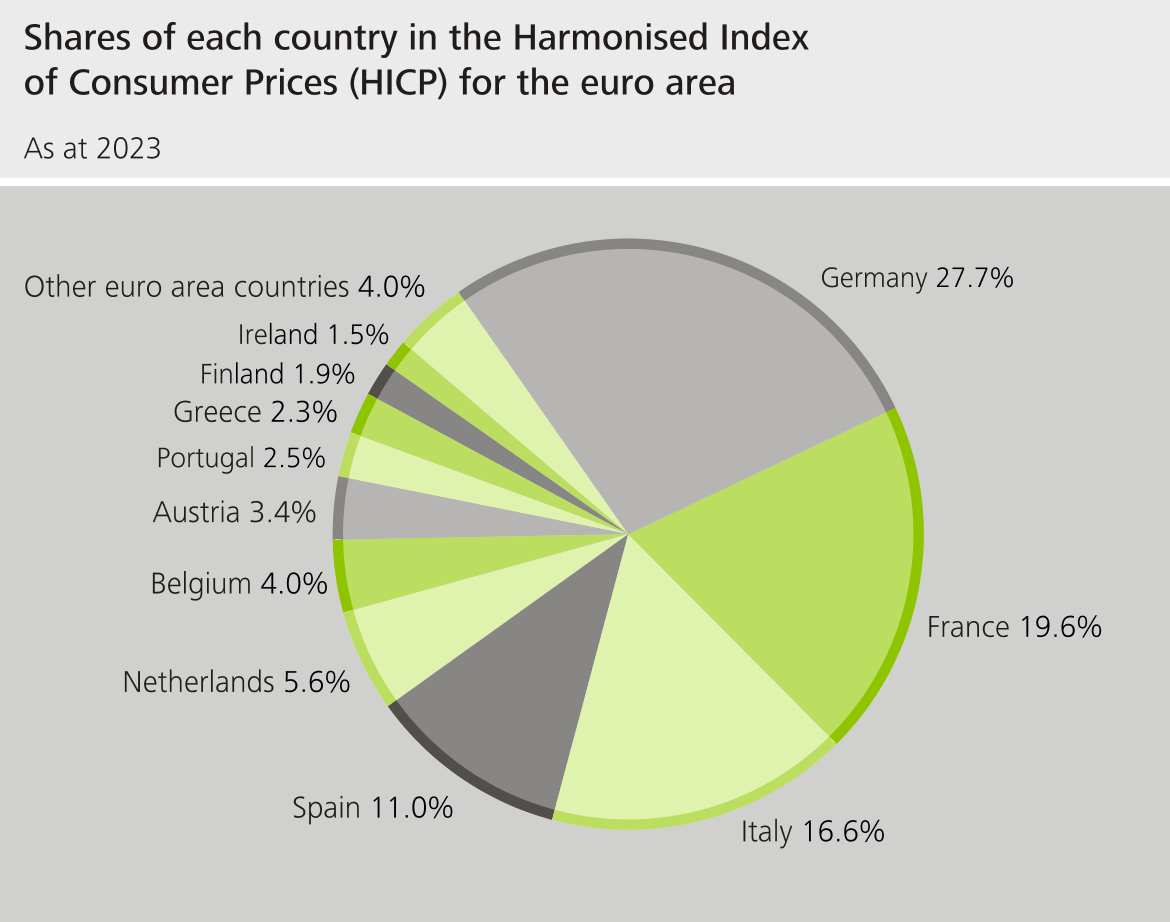

The individual euro area countries report their monthly HICP results to the statistical office of the European Union (Eurostat), which then uses these statistics to calculate the HICP for the euro area. This means that it is neither the Governing Council of the ECB nor the Eurosystem that ascertain price developments, but Eurostat, the European statistical office, which is independent from the central bank. The aggregation of country data into the euro area HICP takes into account the share of each country in overall consumer spending in the euro area. This means that national inflation data are incorporated into the euro area HICP with different weights.

The rate of change in the HICP compared with the same month of the previous year represents the inflation rate in the euro area. The HICP thus also acts as the public’s yardstick for assessing whether the Eurosystem is succeeding in maintaining price stability and thus fulfilling its statutory mandate. The HICP has proven to be a reliable measure of inflation since the beginning of monetary union, and the Governing Council of the ECB underscored its suitability once again in the summer of 2021. At the same time, it made a recommendation to refine the index by including costs of owner-occupied housing in the calculation in future.

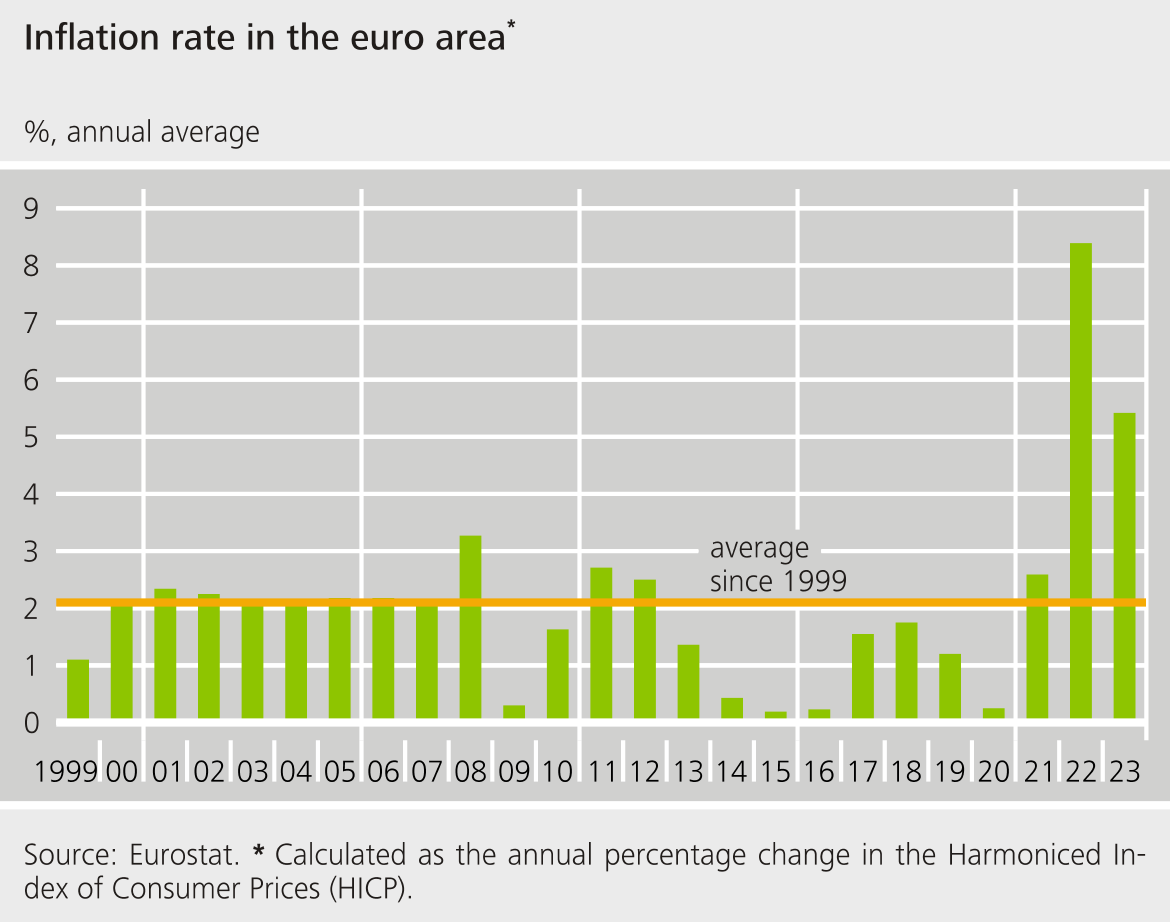

Development of the inflation rate in the euro area

Since the introduction of the euro, annual inflation in the euro area has fluctuated from one year to the next. In 2008, inflation was driven up by higher energy prices, in particular, but just one year later the slump in global economic activity caused by the financial crisis led to a sharp decline in inflationary pressures. The price level even declined in the second half of 2009 for a short period of time.

In the years after 2012, falling energy prices were the main factor behind the clear decline in the inflation rate in the euro area. Added to this was the economic crisis in some euro area countries, which likewise considerably dampened price pressures. In 2015 and 2016, the rate of inflation was only 0.2%, meaning that the price level in the euro area remained virtually unchanged on the previous year. Inflation was also very low in 2020, reflecting the economic downturn caused by the coronavirus pandemic. However, the following year already saw supply-side bottlenecks and surging energy prices causing significantly higher general price pressures. Over the course of 2022, the inflation rate continued to rise, reaching 10% in the autumn. In order to dampen inflation, the Governing Council of the ECB started raising key interest rates in July 2022.

The inflation rates of the individual member countries often differ from the euro area average. Amongst other things, these deviations reflect the fact that economic developments vary across the individual countries. For example, whilst one country is experiencing an economic upswing with falling unemployment and higher wage and price pressures, another country may see a deterioration in economic developments with rising unemployment and declining inflation.